Credit Cards are interesting.

They give you rewards.

Cashback.

Airport lounge access.

And sometimes...

A financial headache you definitely didn't order.

At FinnDot, we like Credit Cards.

When used wisely.

But when the bill keeps rolling into the next month, something dangerous begins.

Interest.

And Credit Card interest doesn't walk.

It runs.

Imagine This...

You spend ₹1 lakh on your Credit Card.

You can't pay the full bill.

So you pay the minimum amount due.

Feels responsible, right?

Not exactly.

The remaining balance starts attracting interest.

Credit Card interest rates can be extremely high.

And suddenly...

You're not just paying for what you bought.

You're paying for the privilege of not paying for it earlier.

What the Finn? 💳

So how do you get out?

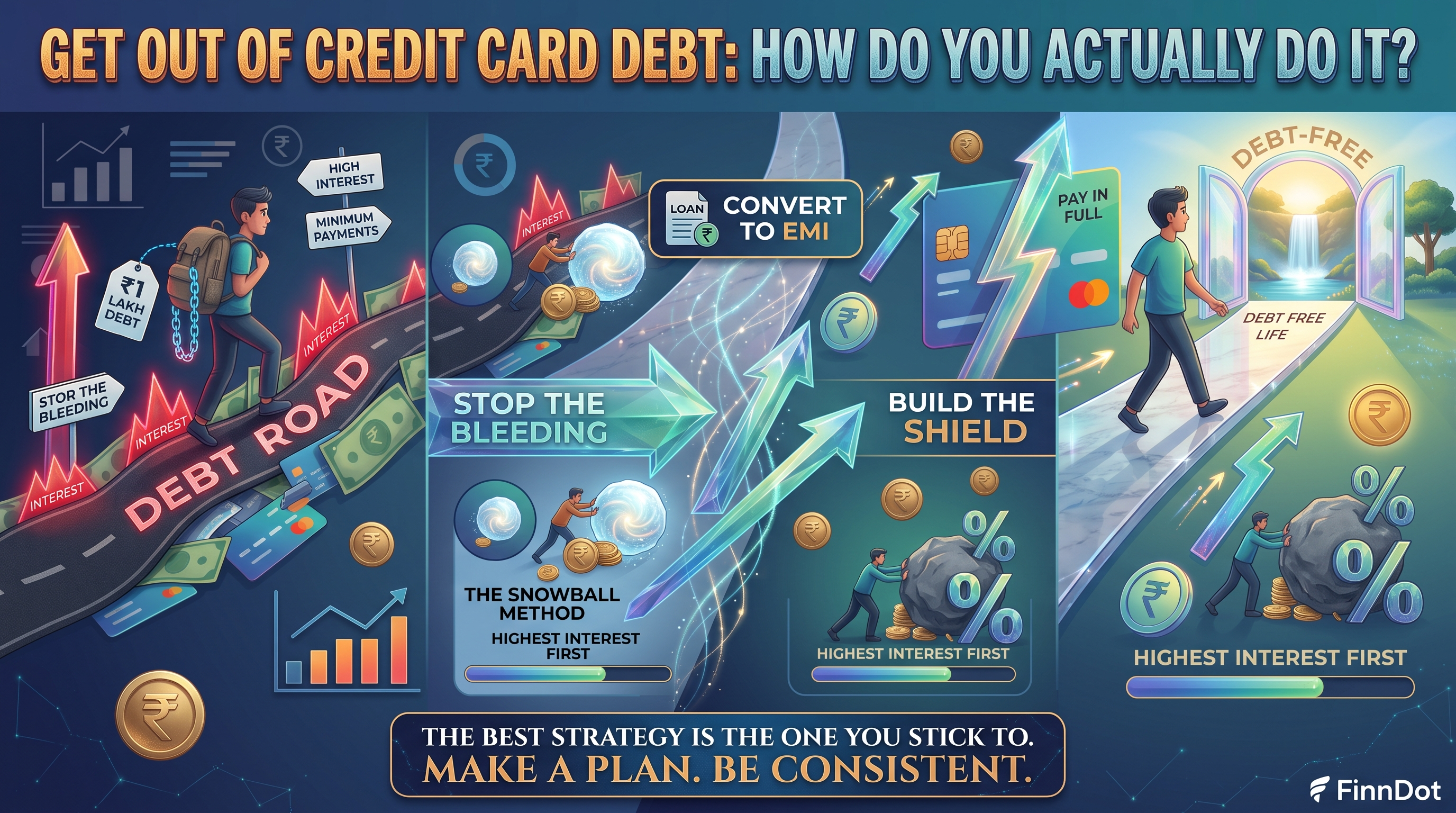

Strategy 1: Convert Your Balance Into EMI

If you can't pay your Credit Card bill in full, check whether your bank allows you to convert the outstanding balance into EMIs.

Why?

Because Credit Card interest can be expensive.

An EMI may offer a lower interest rate and fixed monthly payments.

Instead of fighting a growing bill every month...

You get a repayment plan.

Predictable.

Structured.

Less chaotic.

But check the interest rate and processing fees before converting.

Lower doesn't always mean cheap.

Strategy 2: The Debt Snowball ❄️

Imagine you have three Credit Card debts:

₹10,000

₹40,000

₹80,000

The Snowball Method says:

Attack the ₹10,000 debt first.

Pay the minimum amount on the other cards.

Put every extra rupee toward the smallest debt.

Once it's gone...

Move to ₹40,000.

Then ₹80,000.

Why does this work?

Psychology.

Small wins feel good.

And progress keeps you moving.

Sometimes the best financial strategy isn't mathematically perfect.

It's the one you actually follow.

Strategy 3: The Debt Avalanche 🏔️

Now let's change the game.

Instead of looking at the debt amount...

Look at the interest rate.

Suppose your cards charge:

18%

30%

42%

The Avalanche Method says:

Attack the 42% debt first.

Then 30%.

Then 18%.

Why?

Because the most expensive debt is costing you the most money.

This method may feel slower.

But mathematically...

It can save you more interest.

Snowball or Avalanche?

Simple.

Need motivation?

Choose Snowball.

Want to save more on interest?

Choose Avalanche.

And yes...

You can mix them.

Pay off one small debt for momentum.

Then attack the highest-interest debt.

Personal finance is personal.

The best strategy is the one you can stick to.

But Repaying Debt Is Only Half the Story...

If you keep spending while trying to clear debt...

You're filling a bucket with a hole in it.

Create a budget.

Cut unnecessary spending temporarily.

Use bonuses or extra income to reduce high-interest debt.

And build a small emergency fund.

Because without emergency savings...

Every surprise expense becomes another Credit Card swipe.

Laptop repair?

Swipe.

Medical expense?

Swipe.

Unexpected travel?

Swipe.

And suddenly...

You're back where you started.

Should You Invest While You Have Credit Card Debt?

Suppose your investment earns 12%.

But your Credit Card charges 36%.

You're earning ₹12 on one side...

And losing ₹36 on the other.

That's not investing.

That's financial cardio.

In many cases, clearing high-interest Credit Card debt should come before aggressive investing.

So... Are Credit Cards Bad?

No.

A Credit Card is a tool.

Used well...

It can give you rewards, convenience, and help build your credit history.

Used badly...

It can turn tomorrow's income into yesterday's spending.

The rule is simple.

Spend only what you can afford to repay.

Pay the full bill whenever possible.

Set payment reminders or automatic payments.

And never treat your Credit Card limit as extra income.

Because it isn't your money.

It's borrowed money wearing a very attractive cashback offer.

What the Finn? 💳

Credit Card debt doesn't usually become a problem overnight.

It grows quietly.

One minimum payment.

One carried balance.

One "I'll clear it next month."

And then interest joins the conversation.

The good news?

Debt can be tackled.

Choose a strategy.

Make a plan.

Stay consistent.

Because the goal isn't to fear Credit Cards.

It's to make sure you're using the card...

And the card isn't using you.